Home equity loan rates today sets the stage for this enthralling narrative, offering readers a glimpse into a story that is rich in detail and brimming with originality from the outset. Exploring the intricacies of home equity loan rates can provide valuable insights for those navigating the world of borrowing and lending.

Overview of Home Equity Loan Rates Today

Home equity loan rates refer to the interest rates that borrowers pay when borrowing against the equity in their homes. These rates can vary depending on various factors and can have a significant impact on the overall cost of borrowing.

Types of Home Equity Loan Rates

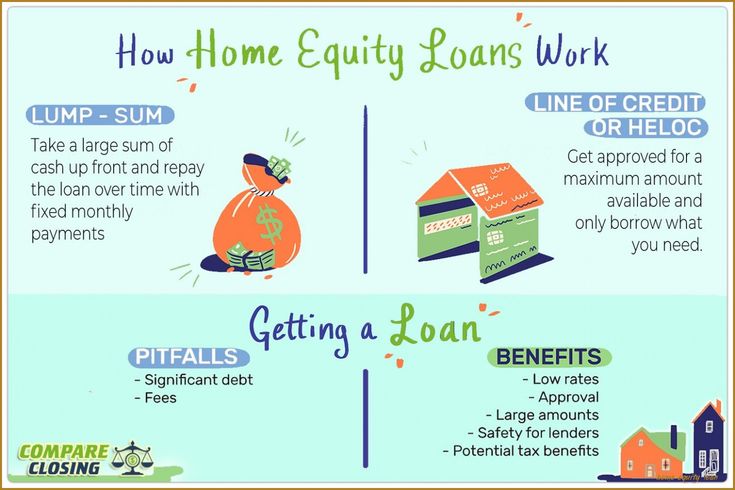

- Fixed-Rate Home Equity Loans: These loans have a fixed interest rate for the entire term of the loan, providing predictability in monthly payments.

- Variable-Rate Home Equity Loans: Also known as adjustable-rate loans, these loans have interest rates that can fluctuate based on market conditions, potentially leading to lower initial rates but higher uncertainty.

- Home Equity Lines of Credit (HELOCs): HELOCs typically have variable interest rates and allow borrowers to draw funds as needed up to a certain limit, making them flexible but subject to interest rate changes.

Determination of Home Equity Loan Rates

Home equity loan rates are determined by lenders based on several factors, including the borrower’s credit score, loan-to-value ratio, the prime rate set by the Federal Reserve, and the overall economic environment. Lenders may also consider the borrower’s income, debt-to-income ratio, and the amount of equity in the home when setting the interest rate.

Factors Influencing Home Equity Loan Rates

When it comes to home equity loan rates today, several key factors play a significant role in determining the interest rates borrowers will receive. Understanding these factors is crucial for individuals considering taking out a home equity loan.

Credit Scores Impact

Credit scores are a major factor that influences home equity loan rates. Borrowers with higher credit scores typically receive lower interest rates, as they are considered less risky by lenders. On the other hand, individuals with lower credit scores may face higher interest rates or even struggle to qualify for a home equity loan.

Loan-to-Value Ratio Influence

The loan-to-value (LTV) ratio is another important factor that affects home equity loan rates. Lenders consider the ratio of the loan amount to the appraised value of the property when determining interest rates. A lower LTV ratio, indicating more equity in the property, can lead to better loan terms and lower interest rates.

Loan Terms Impact

Different loan terms, such as fixed-rate and adjustable-rate loans, can have varying effects on home equity loan rates. Fixed-rate loans provide borrowers with a stable interest rate throughout the loan term, while adjustable-rate loans may offer lower initial rates that can change over time based on market conditions.

Market Conditions Role

Market conditions also play a crucial role in determining home equity loan rates. Factors like the overall economy, inflation rates, and the Federal Reserve’s monetary policy can impact interest rates. Borrowers should stay informed about current market conditions to understand how they may affect their home equity loan rates.

Lender Variance

Different lenders, such as banks and credit unions, may offer varying rates for home equity loans. It is essential for borrowers to compare offers from multiple lenders to find the best rates and terms. Factors like the lender’s risk assessment, operational costs, and competition in the market can lead to differences in interest rates.

Comparison of Fixed vs. Variable Home Equity Loan Rates

When it comes to home equity loan rates, borrowers often have the choice between fixed and variable rates. Each option comes with its own set of advantages and disadvantages, depending on the borrower’s financial situation and market conditions.

Fixed rates offer stability and predictability. The interest rate remains the same throughout the life of the loan, providing borrowers with consistent monthly payments. This can be advantageous when interest rates are low, as borrowers can lock in a favorable rate and protect themselves from potential rate hikes in the future.

On the other hand, variable rates fluctuate based on market conditions. While initial rates may be lower than fixed rates, there is a risk that rates could increase over time, leading to higher monthly payments. Variable rates are typically tied to a benchmark index, such as the prime rate, and can adjust periodically.

When Fixed Rates are More Favorable

- During periods of low interest rates, fixed rates can offer peace of mind and protection against rising rates.

- For borrowers who prefer the certainty of knowing exactly how much they will pay each month.

- When planning for long-term financial stability and budgeting purposes.

Benefits and Drawbacks of Each Type of Rate

| Fixed Rates | Variable Rates |

|---|---|

| Stability and predictability | Potential for lower initial rates |

| Protection against rising interest rates | Risk of rates increasing over time |

| Consistent monthly payments | Monthly payments can fluctuate |

Current Trends in Home Equity Loan Rates

As of the latest data available, the national average home equity loan rate is X.XX%. This rate can vary depending on individual lenders and borrowers’ creditworthiness.

Recent Changes in Home Equity Loan Rates

- Over the past 6 months, home equity loan rates have seen a slight increase due to the overall rise in interest rates in the market.

- Lenders have adjusted their rates to reflect the changing economic landscape and increased demand for home equity loans.

Impact of Economic Factors on Home Equity Loan Rates

- The Federal Reserve’s decisions on interest rates play a crucial role in determining home equity loan rates.

- If the Federal Reserve increases interest rates, home equity loan rates are likely to follow suit, making borrowing more expensive for homeowners.

Comparison of Fixed-Rate and Variable-Rate Home Equity Loans

Currently, fixed-rate home equity loans are more popular among borrowers due to their predictability and stability. The current average rate for a fixed-rate home equity loan is X.XX%.

On the other hand, variable-rate home equity loans have lower initial rates but can fluctuate over time based on market conditions. The current average rate for a variable-rate home equity loan is X.XX%.

Understanding APR vs. Interest Rates for Home Equity Loans

When considering home equity loans, it is essential to understand the difference between APR and interest rates to make informed financial decisions.

Calculation of APR and Interest Rates

APR includes the interest rate as well as additional fees and costs associated with the loan, giving a more comprehensive view of the total cost of borrowing. On the other hand, the interest rate only represents the percentage of the principal amount charged for borrowing.

Importance of Understanding APR

Comparing APRs for different home equity loan offers allows borrowers to accurately assess the total cost of borrowing, including fees and other charges. This helps in making a more informed decision and avoiding any hidden costs.

| Loan Offer | Interest Rate | APR |

|---|---|---|

| Offer 1 | 4.5% | 5.0% |

| Offer 2 | 4.8% | 5.3% |

A lower APR can save borrowers money over time by reducing the total cost of borrowing, including fees and charges, leading to lower monthly payments.

Calculating Total Cost of Home Equity Loan

- Step 1: Convert the APR to a monthly periodic rate by dividing it by 12.

- Step 2: Calculate the monthly interest payment by multiplying the monthly rate by the outstanding balance.

- Step 3: Add any additional fees or charges to the monthly interest payment to get the total monthly payment.

- Step 4: Multiply the total monthly payment by the loan term in months to get the total cost of the loan.

Shopping Around for the Best Home Equity Loan Rates Today

When looking for the best home equity loan rates, it’s essential to shop around and compare different options to ensure you’re getting the most favorable terms for your financial needs.

Comparing Different Home Equity Loan Rates

- Start by researching and comparing interest rates offered by various lenders, including banks, credit unions, and online lenders.

- Consider the loan terms, repayment options, and any associated fees or closing costs that could affect the overall cost of the loan.

- Use online tools and resources to compare loan offers side by side and calculate the total cost of borrowing to make an informed decision.

Looking Beyond Interest Rates

- While interest rates are crucial, also consider the lender’s reputation, customer service, and flexibility in case of financial hardships or changes in circumstances.

- Pay attention to the loan-to-value ratio requirements, as well as any prepayment penalties or restrictions that could impact your ability to pay off the loan early.

Factors to Consider When Shopping for the Best Home Equity Loan Rates

- Loan term and repayment schedule

- Total cost of borrowing, including fees and closing costs

- Lender’s reputation and customer service

- Loan-to-value ratio requirements

- Prepayment penalties or restrictions

Impact of Credit Scores on Loan Rates

- Higher credit scores typically result in lower interest rates offered by lenders, while lower scores may lead to higher rates or difficulty in securing a loan.

- Improving your credit score before applying for a home equity loan can help you qualify for better rates and terms.

Fixed-Rate vs. Variable-Rate Home Equity Loans

- Fixed-rate loans offer stable monthly payments and protection against interest rate fluctuations, while variable-rate loans may have lower initial rates but can increase over time.

- Consider your financial goals, risk tolerance, and the current interest rate environment when choosing between fixed and variable-rate options.

Platforms for Comparing Home Equity Loan Rates

- Popular financial institutions like Wells Fargo, Chase, and Bank of America offer tools to compare home equity loan rates and terms online.

- Websites like LendingTree, Bankrate, and NerdWallet provide comparison tools and resources to help you find the best home equity loan rates available.

Impact of Federal Reserve Rates on Home Equity Loan Rates

The Federal Reserve plays a significant role in influencing the interest rates that financial institutions charge for home equity loans. Changes in the Federal Reserve rates can have a direct impact on the rates borrowers can expect to pay for their home equity loans.

Relationship between Federal Reserve Rates and Home Equity Loan Rates

The Federal Reserve sets the federal funds rate, which is the interest rate at which banks lend money to each other overnight. When the Federal Reserve raises or lowers this rate, it affects the overall cost of borrowing money for financial institutions. As a result, banks may adjust their home equity loan rates in response to changes in the federal funds rate.

- For example, if the Federal Reserve increases interest rates, banks may raise their home equity loan rates to reflect the higher cost of borrowing for them.

- Conversely, when the Federal Reserve cuts interest rates, banks may lower their home equity loan rates to attract more borrowers and stimulate borrowing.

Recent Examples of Federal Reserve Rate Changes Impacting Home Equity Loan Rates

In recent years, we have seen how changes in Federal Reserve rates have influenced home equity loan rates. For instance, when the Federal Reserve began raising rates in 2018, many banks followed suit by increasing their home equity loan rates. This trend continued until the Federal Reserve started cutting rates in 2019, leading to a decrease in home equity loan rates offered by financial institutions.

Overall, it is essential for borrowers to keep an eye on Federal Reserve rate changes, as they can directly impact the interest rates they are offered for home equity loans. By understanding this relationship, borrowers can make informed decisions about when to take out a home equity loan based on current market conditions.

Risks Associated with Fluctuating Home Equity Loan Rates

When it comes to home equity loans, one of the major risks borrowers face is the fluctuation of interest rates. These fluctuations can impact the cost of borrowing, monthly payments, and overall financial stability. It’s essential for borrowers to understand these risks and be prepared to manage them effectively.

Identifying Potential Risks

One of the main risks associated with fluctuating home equity loan rates is the potential for increased monthly payments. If interest rates rise, borrowers may find themselves paying more each month, which can strain their finances. Additionally, fluctuating rates can make it challenging to budget effectively, as the cost of borrowing can vary unpredictably.

Strategies for Managing Risks

– Consider opting for a fixed-rate home equity loan to provide stability in monthly payments, even if interest rates rise in the future.

– Keep an eye on market trends and consider refinancing if interest rates drop significantly to take advantage of lower rates.

– Create a financial cushion by setting aside savings to cover potential increases in monthly payments due to fluctuating interest rates.

Protecting Against Adverse Rate Fluctuations

Borrowers can protect themselves from adverse rate fluctuations by:

– Monitoring interest rate trends and being proactive in adjusting their loan terms if necessary.

– Consulting with a financial advisor to understand the implications of fluctuating rates on their specific financial situation.

– Making extra payments towards the principal of the loan to reduce the impact of rising interest rates on the overall cost of borrowing.

Eligibility Criteria for Securing Competitive Home Equity Loan Rates

When it comes to securing competitive home equity loan rates, meeting the eligibility criteria is crucial. Lenders consider various factors to determine the interest rate you qualify for. Understanding these criteria and knowing how to improve your eligibility can help you secure better rates.

Common Eligibility Requirements

- Stable Income: Lenders typically look for a steady source of income to ensure you can repay the loan.

- Good Credit History: A strong credit score demonstrates your ability to manage debt responsibly and can result in lower interest rates.

- Sufficient Home Equity: The value of your home and the amount of equity you have built up play a significant role in determining the loan amount and interest rate.

Factors Impacting Eligibility

- Income: Higher income levels can make you a more attractive borrower, potentially leading to lower interest rates.

- Credit History: A good credit score indicates financial responsibility and can result in better loan terms.

- Home Equity Value: The more equity you have in your home, the more favorable rates you may qualify for.

Tips for Improving Eligibility

- Pay off existing debt to improve your debt-to-income ratio.

- Check your credit report for errors and work on improving your credit score.

- Increase the equity in your home by making extra mortgage payments or completing home improvements.

Home Equity Loan Rate Calculators and Tools

When exploring options for a home equity loan, utilizing online calculators and tools can be incredibly helpful in estimating potential rates and payments. These resources provide borrowers with valuable insights into their financial commitments and help them make informed decisions.

Benefits of Using Rate Calculators for Borrowers

- Allows borrowers to estimate monthly payments based on different loan amounts and interest rates

- Helps in comparing various loan options to find the most suitable one

- Provides a clear understanding of the financial implications of taking out a home equity loan

Step-by-Step Guide on How to Use a Home Equity Loan Rate Calculator Effectively

- Enter the loan amount you are considering

- Add the estimated interest rate provided by the lender

- Include other relevant details such as loan term and any additional fees

- Review the calculated monthly payments and total interest to make an informed decision

Key Factors Influencing Home Equity Loan Rates

- Credit Score: Higher credit scores typically result in lower interest rates

- Loan Amount: Larger loan amounts may come with higher interest rates

- Loan-to-Value Ratio: Lower ratios often lead to better loan terms

Comparison Table of Different Home Equity Loan Calculators

| Calculator | Features |

|---|---|

| Calculator A | Allows for comparison between fixed and variable rates |

| Calculator B | Provides a breakdown of monthly payments and total interest over the loan term |

Common Terminology Related to Home Equity Loans

- APR: Annual Percentage Rate, including interest and fees

- Fixed Rate: Interest rate that remains the same throughout the loan term

- Adjustable Rate: Interest rate that can fluctuate based on market conditions

- Repayment Terms: Conditions outlining how the loan will be repaid

Tips on Interpreting Results from a Home Equity Loan Rate Calculator

- Consider the total cost of the loan, including interest and fees

- Review the monthly payments to ensure they fit within your budget

- Compare multiple loan options to find the most favorable terms

Case Studies

In this section, we will delve into real-life scenarios of home equity loan rates today, analyzing different factors that influence these rates and the outcomes of each case study.

Case Study 1: Urban vs. Rural Home Equity Loan Rates

- Urban Area: The home equity loan rates in urban areas tend to be slightly higher due to the higher demand for properties and the cost of living.

- Rural Area: In rural areas, home equity loan rates are typically lower as the demand for properties is lower and the cost of living is generally cheaper.

Case Study 2: Credit Score Impact on Home Equity Loan Rates

- High Credit Score: Borrowers with a high credit score are more likely to secure lower home equity loan rates due to their creditworthiness.

- Low Credit Score: Conversely, borrowers with a low credit score may face higher home equity loan rates as they are considered higher risk by lenders.

Case Study 3: Economic Conditions and Home Equity Loan Rates

- During Economic Boom: In times of economic prosperity, home equity loan rates may increase as demand for loans rises.

- During Economic Downturn: Conversely, in economic downturns, home equity loan rates may decrease as lenders compete for borrowers amid lower demand.

Experts suggest that borrowers should closely monitor economic trends and their credit score to secure the best home equity loan rates.

Comparative Analysis Table

| Factors | Urban Area | Rural Area | High Credit Score | Low Credit Score | Economic Boom | Economic Downturn |

|---|---|---|---|---|---|---|

| Interest Rates | Higher | Lower | Lower | Higher | Higher | Lower |

Graphs Illustrating Fluctuation of Home Equity Loan Rates

Visual aids such as graphs can provide a clear representation of how home equity loan rates fluctuate over time in different scenarios.

Expert Insights on Predicting Future Home Equity Loan Rates

When it comes to predicting future home equity loan rates, industry experts specializing in financial forecasting play a crucial role in providing valuable insights. By analyzing various economic indicators and data points, these experts can offer valuable predictions regarding the trajectory of home equity loan rates.

Economic Indicators and Data Points for Forecasting Home Equity Loan Rates

- Experts often look at the performance of the housing market as a key indicator for predicting home equity loan rates. A strong housing market usually correlates with lower rates, while a weakening market may lead to rate increases.

- Interest rate movements, especially those set by the Federal Reserve, are closely monitored by experts. Changes in interest rates can directly impact home equity loan rates, making it essential to consider when forecasting future trends.

- Economic growth projections also play a significant role in predicting home equity loan rates. A growing economy typically leads to lower rates, while a stagnant or declining economy may result in rate hikes.

Impact of External Factors on Home Equity Loan Rates

- Government policies and regulations can heavily influence the direction of home equity loan rates. Changes in tax laws or housing initiatives can either lower or raise rates, depending on their impact on the overall market.

- Global economic conditions, such as trade agreements and geopolitical events, can also have a ripple effect on home equity loan rates. Experts must consider these external factors when making predictions about future rate trends.

Technologies and Methodologies for Rate Predictions

- Experts are increasingly turning to advanced technologies like machine learning and predictive analytics to enhance the accuracy of their rate predictions. These tools can analyze vast amounts of data and identify patterns that human analysts may overlook.

- By leveraging these emerging technologies, experts can provide more precise forecasts regarding home equity loan rates, helping borrowers make informed decisions about their financial future.

Strategies for Borrowers in Response to Rate Trends

- Borrowers can take advantage of favorable rate trends by locking in a fixed-rate home equity loan when rates are low. This provides stability and protection against potential rate increases in the future.

- Monitoring economic indicators and staying informed about market trends can help borrowers anticipate rate changes and adjust their financial strategy accordingly. By being proactive, borrowers can position themselves to benefit from favorable rate environments.

Tips for Negotiating Better Home Equity Loan Rates

When it comes to securing a home equity loan, negotiating for better rates can lead to significant savings over the life of the loan. By leveraging certain factors and employing smart negotiation tactics, borrowers can potentially lower their home equity loan rates and reduce their overall borrowing costs.

Understand Your Financial Situation

- Before negotiating with lenders, take the time to assess your financial situation. Understand your credit score, debt-to-income ratio, and overall financial health to determine your negotiating power.

- Having a strong credit score and a stable income can help you negotiate for better rates, as lenders are more likely to offer favorable terms to low-risk borrowers.

Shop Around and Compare Offers

- Don’t settle for the first offer you receive. Shop around and compare home equity loan rates from multiple lenders to get a sense of the market and identify competitive rates.

- Consider using online tools and resources to compare offers side by side, helping you make informed decisions and negotiate effectively.

Highlight Your Loyalty and Relationship with the Lender

- If you have an existing relationship with a lender, leverage that loyalty to negotiate better rates. Lenders may be willing to offer discounts or lower rates to retain your business.

- Show your commitment to the lender by consolidating accounts or services, which can strengthen your negotiating position and lead to more favorable terms.

Negotiate Fees and Terms

- In addition to interest rates, don’t forget to negotiate fees and terms associated with the home equity loan. Ask about waiving origination fees, reducing closing costs, or adjusting repayment terms to better suit your financial needs.

- Be prepared to negotiate on multiple fronts, including interest rates, fees, and repayment terms, to secure the best overall package for your home equity loan.

Closure

As we conclude this discussion on home equity loan rates today, it becomes evident that staying informed and proactive is key to making sound financial decisions. Whether you’re a seasoned borrower or a first-time applicant, understanding the nuances of home equity loan rates can empower you to secure favorable terms and achieve your financial goals with confidence.