5 year home equity loan rates sets the stage for this enthralling narrative, offering readers a glimpse into a story that is rich in detail and brimming with originality from the outset. In this comprehensive guide, we will delve into the intricacies of 5-year home equity loans, exploring everything from interest rate determinants to potential risks and tax implications.

For those seeking clarity on how to secure the best rates and navigate the world of home equity loans, this exploration of 5-year options is sure to provide valuable insights and guidance.

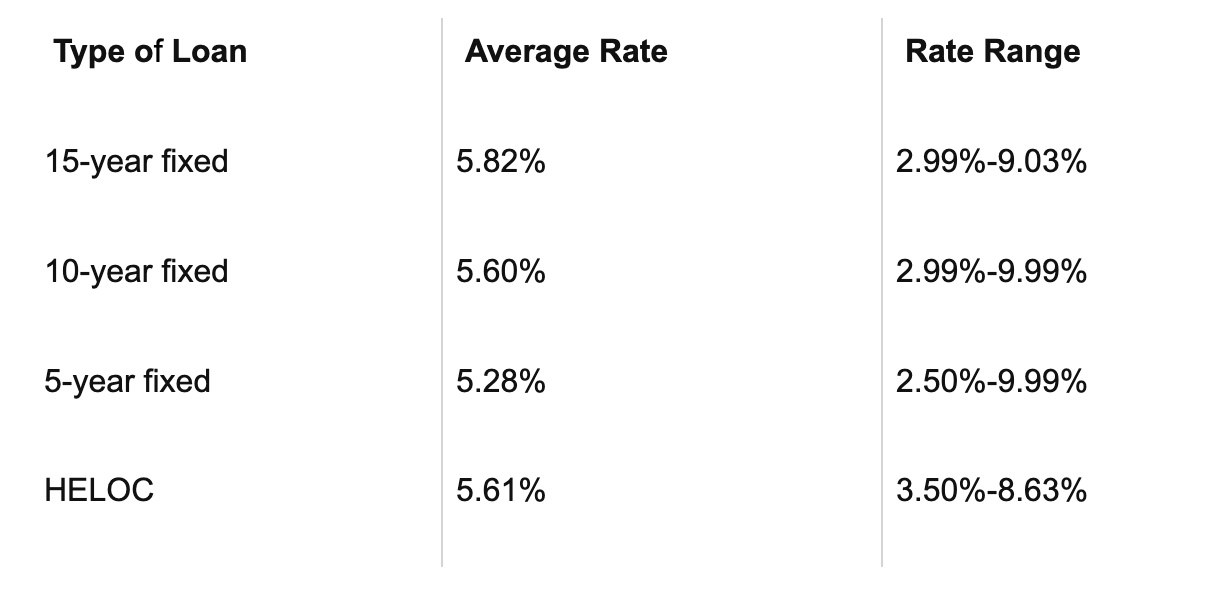

Overview of 5-year home equity loan rates

A 5-year home equity loan is a type of loan where homeowners can borrow money using the equity in their home as collateral. The loan is typically repaid over a period of five years with fixed monthly payments.

How interest rates are determined for these loans

Interest rates for 5-year home equity loans are determined based on factors such as the borrower’s credit score, loan amount, loan-to-value ratio, and current market conditions. Lenders may also consider the prime rate set by the Federal Reserve when determining interest rates.

Comparison with other loan options

Compared to other loan options such as personal loans or credit cards, 5-year home equity loans generally offer lower interest rates since they are secured by the home’s equity. However, borrowers risk losing their home if they fail to repay the loan.

Qualifying for a 5-year home equity loan

To qualify for a 5-year home equity loan, borrowers typically need a good credit score, sufficient equity in their home, and a stable income. Lenders may also require a debt-to-income ratio within a certain range and may conduct a home appraisal.

Average interest rates from different lenders

Below is a table showing the average interest rates for 5-year home equity loans from various lenders:

| Lender | Average Interest Rate |

|—————-|———————–|

| Bank A | 3.5% |

| Credit Union B | 4.0% |

| Online Lender C | 3.75% |

Potential risks of taking out a 5-year home equity loan

One of the main risks of taking out a 5-year home equity loan is the possibility of foreclosure if the borrower defaults on the loan. Additionally, if property values decline, borrowers may end up owing more than their home is worth.

Tax implications of using a 5-year home equity loan

The interest paid on a 5-year home equity loan may be tax-deductible if the funds are used to improve the home. However, if the funds are used for other purposes such as debt consolidation or vacations, the interest may not be tax-deductible. It is important for borrowers to consult with a tax advisor to understand the specific tax implications in their situation.

Factors influencing 5-year home equity loan rates

When it comes to 5-year home equity loan rates, various factors come into play that can impact the interest rates offered to borrowers. Understanding these key factors is essential for individuals looking to secure the best possible rate for their financial situation.

One crucial factor that significantly influences 5-year home equity loan rates is the borrower’s credit score. Lenders use credit scores to assess the borrower’s creditworthiness and determine the level of risk associated with lending money. A higher credit score typically results in lower interest rates, as it signals to lenders that the borrower is more likely to repay the loan on time. On the other hand, a lower credit score may lead to higher interest rates or even difficulty in securing a loan.

Another important factor that plays a role in determining 5-year home equity loan rates is the loan-to-value (LTV) ratio. This ratio compares the amount of the loan to the appraised value of the property. A lower LTV ratio indicates that the borrower has more equity in their home, which can result in lower interest rates. Conversely, a higher LTV ratio may lead to higher interest rates or additional requirements from the lender to mitigate the increased risk.

Credit Scores and Loan Rates

When it comes to 5-year home equity loan rates, credit scores play a significant role in determining the interest rates offered to borrowers. Here’s how credit scores can impact loan rates:

- Borrowers with excellent credit scores (above 800) are likely to qualify for the lowest interest rates available.

- Individuals with good credit scores (around 700-799) may still qualify for competitive rates, although slightly higher than those with excellent credit.

- For borrowers with fair to poor credit scores (below 700), interest rates may be higher, and they may face challenges in securing a loan.

Loan-to-Value Ratios and Interest Rates

The loan-to-value (LTV) ratio is another critical factor that influences 5-year home equity loan rates. Here’s how LTV ratios can impact interest rates:

- A lower LTV ratio, indicating more equity in the property, can lead to lower interest rates and more favorable loan terms.

- Higher LTV ratios, on the other hand, may result in higher interest rates, as lenders perceive increased risk due to less equity in the property.

- Borrowers with high LTV ratios may need to meet additional requirements or pay higher rates to offset the risk for the lender.

Pros and cons of choosing a 5-year term for a home equity loan

When considering a 5-year term for a home equity loan, there are several advantages and disadvantages to take into account.

Advantages of a 5-year term:

- Interest savings: Opting for a shorter loan term can result in significant interest savings over the life of the loan, as less time means less interest accrued.

- Quicker debt repayment: A 5-year term allows you to pay off your loan faster, helping you build equity in your home sooner.

- Potentially lower interest rates: Shorter loan terms often come with lower interest rates, saving you money in interest payments.

Disadvantages of a 5-year term:

- Higher monthly payments: With a shorter loan term, your monthly payments will be higher compared to longer-term options, which could strain your budget.

- Limited flexibility in budgeting: The higher monthly payments of a 5-year term may limit your ability to allocate funds to other expenses or savings goals.

Comparison with longer-term options:

When comparing a 5-year term with longer-term options like 10 or 15 years, it’s important to consider the total interest paid, overall cost, and alignment with your financial goals.

Assessing personal financial situation:

- Consider your income stability and cash flow to determine if you can comfortably afford the higher monthly payments of a 5-year term.

- Evaluate your long-term financial goals and timeline to see if a shorter loan term aligns with your objectives, such as paying off debt before retirement or saving for other major expenses.

Comparison of fixed vs. adjustable rates for 5-year home equity loans

When considering a 5-year home equity loan, borrowers often have to choose between fixed and adjustable rates. Each option comes with its own set of advantages and disadvantages, making it essential to understand the differences before making a decision.

Fixed Rate:

Fixed-rate loans offer stability and predictability as the interest rate remains constant throughout the loan term. This means that your monthly payments will not change, providing a sense of security for budgeting purposes. Fixed rates are ideal for borrowers who prefer consistency and want to avoid the risk of rising interest rates in the future.

Adjustable Rate:

Adjustable-rate loans, also known as variable-rate loans, have interest rates that can fluctuate over time based on market conditions. While initial rates may be lower than fixed rates, there is a risk of rates increasing in the future, leading to higher monthly payments. Adjustable rates offer flexibility and the potential for lower initial payments, making them suitable for borrowers who are comfortable with some level of uncertainty and are willing to take on the risk of rate changes.

Scenarios:

– Fixed rates may be more beneficial for borrowers who prioritize stability and want to lock in a low rate for the entire loan term.

– Adjustable rates may be advantageous for borrowers who plan to sell or refinance their home within a few years, as they can take advantage of lower initial rates without being overly concerned about future rate adjustments.

When Fixed Rates are Preferred

- Fixed rates provide peace of mind and security in knowing that monthly payments will not change.

- Borrowers who intend to stay in their homes for the long term may benefit from fixed rates to avoid potential rate hikes.

When Adjustable Rates are Preferred

- Adjustable rates can offer lower initial payments, making them attractive for borrowers with short-term homeownership plans.

- Borrowers who expect interest rates to decrease in the future may opt for adjustable rates to take advantage of potential savings.

Understanding APR vs. interest rate for 5-year home equity loans

When considering a 5-year home equity loan, it’s essential to understand the difference between APR and interest rate to make informed borrowing decisions.

Definition of APR and its Impact

The Annual Percentage Rate (APR) includes the interest rate and other fees charged by the lender, such as closing costs, points, and origination fees. It provides a more comprehensive view of the total cost of borrowing compared to the interest rate alone.

Significance of APR in Loan Decisions

- APR impacts the total amount you will repay over the loan term.

- A lower APR typically means lower overall borrowing costs.

- Comparing APRs among lenders can help you choose the most cost-effective loan option.

Factors Influencing APR on Home Equity Loans

- Current market interest rates.

- Your credit score and financial history.

- The loan amount and term.

- Lender fees and policies.

Comparison of High APR vs. High-Interest Rate

A high APR can result from additional fees, while a high-interest rate indicates higher borrowing costs. It’s crucial to consider both factors when evaluating loan options to understand the total cost of borrowing.

Hypothetical Home Equity Loan Scenario

| APR | Interest Rate | Total Amount Repaid |

|---|---|---|

| 4% | 3.5% | $50,000 |

| 5% | 4.5% | $52,500 |

| 6% | 5.5% | $55,000 |

Annual Percentage Yield (APY) Explained

The APY takes into account the effect of compounding interest on your investment or loan. It provides a more accurate representation of the actual return or cost you will experience over time, considering the frequency of compounding.

Market trends affecting 5-year home equity loan rates

Understanding the market trends that impact 5-year home equity loan rates is crucial for homeowners looking to secure a loan. By analyzing recent trends and economic factors, we can gain insights into potential future changes in interest rates.

Recent Trends in Interest Rates

Over the past 5 years, interest rates for 5-year home equity loans have fluctuated based on various economic indicators. It is essential to track these trends to make informed decisions about loan options.

Economic Factors Influencing Rates

- The Federal Reserve’s monetary policy

- Inflation rates

- Unemployment rates

- GDP growth

- Housing market conditions

Comparative Analysis of Fixed vs. Variable Rates

Comparing fixed and variable rates for 5-year home equity loans over the past 5 years can provide insights into which option may be more beneficial for borrowers. Understanding how these rates have performed historically is essential for decision-making.

Government Policies Impact on Rates

- The impact of government regulations on lending practices

- The role of government-backed loan programs

- Tax policies affecting home equity loan interest deductions

Relationship Between Housing Market Trends and Loan Rates

Fluctuations in the housing market directly impact home equity loan rates. Understanding the relationship between market trends, such as home prices and inventory levels, and loan rates can help borrowers anticipate changes in their borrowing costs.

Comparison of national vs. local 5-year home equity loan rates

When looking at 5-year home equity loan rates, it’s important to consider the difference between national rates and local rates. National rates are the average rates offered across the entire country, while local rates can vary based on the area you are in. Let’s explore how these differences can impact your loan options.

Impact of Location on Home Equity Loan Rates

Local lenders may offer lower rates compared to national institutions due to competition and knowledge of the local market. They may also be more willing to work with borrowers who have unique financial situations or credit histories.

On the other hand, national institutions may offer more consistency and convenience in terms of online services and branch availability. However, their rates may be less competitive than what local lenders can provide.

It can be beneficial to choose local lenders over national institutions when you value personalized service, have specific needs that may not fit traditional lending criteria, or want to take advantage of potentially lower rates based on local market conditions.

Impact of loan term length on 5-year home equity loan rates

When considering a 5-year home equity loan, it is crucial to understand how the loan term length can affect the interest rates, overall costs, and monthly payments. Let’s explore the implications of varying the loan term from 5 to 10 years.

Comparison of 5-year term vs. 10-year term

Extending the loan term from 5 years to 10 years typically results in lower monthly payments but higher overall interest costs. While a 10-year term may offer more flexibility in budgeting, it comes with the trade-off of paying more in interest over the life of the loan.

- Choosing a 5-year term: With a shorter term, borrowers can benefit from lower interest rates and faster equity build-up. Monthly payments are usually higher but result in significant savings on interest payments over time.

- Choosing a 10-year term: Opting for a longer term reduces monthly payments but increases the total interest paid. This can be advantageous for borrowers looking for more affordable monthly payments but may end up paying more in interest over the loan term.

Cost implications and potential savings

When comparing the cost implications of a 5-year term versus a 10-year term, it is essential to consider the total amount paid in interest over the life of the loan. A shorter term may result in higher monthly payments but substantial savings in interest payments.

By choosing a 5-year term over a 10-year term, borrowers can save thousands of dollars in interest payments.

Monthly payment comparison

Let’s break down the differences in monthly payments between a 5-year and a 10-year term to understand the impact on cash flow and budgeting.

| Loan Term | Monthly Payment |

|---|---|

| 5 years | [Monthly payment amount] |

| 10 years | [Monthly payment amount] |

Recommendation based on financial goals

When recommending the most suitable term length for a home equity loan, it is essential to consider the borrower’s overall financial goals. Whether the focus is on paying off the loan quickly, minimizing interest costs, or managing monthly cash flow, the loan term should align with the borrower’s specific objectives and financial situation.

Tips for securing the best 5-year home equity loan rates

When it comes to securing the best 5-year home equity loan rates, there are several strategies that can help you get a better deal. Improving credit scores, negotiating with lenders, and comparing offers are crucial steps in ensuring you get the most favorable terms for your loan.

Strategies for negotiating lower rates with lenders

- Research current market rates and come prepared with this information when negotiating with lenders.

- Highlight your strong credit history, income stability, and the equity in your home to showcase your creditworthiness.

- Consider asking for a lower interest rate in exchange for setting up automatic payments or maintaining a checking account with the lender.

Importance of improving credit scores before applying

- Check your credit report for any errors and work on improving your credit score by paying down debt and making timely payments.

- A higher credit score can help you qualify for lower interest rates, saving you money over the life of the loan.

Guidance on how to compare offers from different lenders effectively

- Request loan estimates from multiple lenders to compare interest rates, closing costs, and fees.

- Consider the APR, which includes both the interest rate and any additional costs associated with the loan, for a more accurate comparison.

- Look beyond the interest rate and consider the overall terms and conditions of the loan, such as prepayment penalties or adjustable rate features.

Case studies highlighting real-life examples of 5-year home equity loan rates

In the following case studies, we will explore various financial profiles and how 5-year home equity loan rates differ based on market fluctuations. Recommendations will be provided based on the outcomes of each scenario.

Case Study 1: Young Couple with Stable Income

- The young couple, both with stable jobs and good credit scores, applied for a 5-year home equity loan to renovate their home.

- Due to the current low market rates, they were able to secure a competitive interest rate of 3.5% APR for their loan.

- Despite the initial uncertainty, the couple decided to lock in the rate, considering the predictability of fixed rates for their budget.

Case Study 2: Retired Individual on Fixed Income

- A retired individual with a fixed income sought a 5-year home equity loan to cover medical expenses.

- Given the fluctuating market trends, the individual faced higher interest rates at 4.5% APR for the loan.

- After careful consideration, the retiree opted for an adjustable-rate loan, hoping for potential rate decreases in the future.

Case Study 3: Small Business Owner Seeking Expansion

- A small business owner wanted to expand operations and utilized a 5-year home equity loan for funding.

- Market fluctuations led to varying rates, with the owner securing a rate of 3.75% APR after consulting with multiple lenders.

- Considering the business growth projections, the owner chose a fixed-rate loan to maintain financial stability over the loan term.

Exploring refinancing options for 5-year home equity loans

When it comes to 5-year home equity loans, refinancing can be a strategic move to secure better rates and potentially reduce monthly payments. By refinancing, homeowners have the opportunity to take advantage of lower interest rates or improved creditworthiness since the original loan was obtained. This can lead to significant savings over the life of the loan.

Benefits of refinancing for 5-year home equity loans

- Lower interest rates: Refinancing can help homeowners secure a lower interest rate, resulting in reduced overall costs.

- Lower monthly payments: With a lower interest rate, monthly payments may decrease, providing more financial flexibility.

- Consolidating debt: Refinancing can also be used to consolidate high-interest debt into a single, more manageable payment.

When to refinance a 5-year home equity loan

- Significant drop in interest rates: If interest rates have significantly decreased since obtaining the original loan, refinancing may be beneficial.

- Improved credit score: A higher credit score can lead to better loan terms, making refinancing a smart choice.

- Financial goals: Refinancing can help homeowners achieve financial goals such as paying off debt or funding home improvements.

Steps to follow when considering refinancing

- Evaluate current loan terms: Understand the terms of your current loan, including interest rate, monthly payments, and remaining balance.

- Check credit score: Review your credit score and take steps to improve it if needed to qualify for better rates.

- Shop around for lenders: Compare offers from multiple lenders to ensure you’re getting the best possible terms.

- Calculate potential savings: Use online calculators or consult with a financial advisor to determine how much you could save by refinancing.

- Submit a refinance application: Once you’ve selected a lender, complete the application process and provide any required documentation.

Regulatory considerations affecting 5-year home equity loan rates

When it comes to 5-year home equity loan rates, regulatory factors play a significant role in determining the interest rates that borrowers will encounter. These regulations are put in place to protect both lenders and borrowers and ensure a fair and transparent lending environment.

Impact of Regulations on Interest Rates

Regulations such as the Truth in Lending Act (TILA) and the Home Mortgage Disclosure Act (HMDA) require lenders to disclose important information to borrowers, including interest rates, fees, and terms. These regulations help borrowers make informed decisions and prevent predatory lending practices. Compliance with these regulations can impact the overall cost of borrowing, including the interest rates offered on home equity loans.

- Regulations like TILA may require lenders to calculate interest rates in a specific way, influencing the rates borrowers receive.

- Regulatory changes can also impact the availability of certain loan products or affect the underwriting criteria used by lenders, which can, in turn, affect interest rates.

- Government agencies like the Consumer Financial Protection Bureau (CFPB) oversee compliance with lending regulations and may take enforcement actions that impact how lenders operate.

Government Policies and Loan Rate Environment

Government policies, such as monetary policy set by the Federal Reserve, can also influence interest rates on home equity loans. The Federal Reserve’s decisions on the federal funds rate can indirectly impact the rates borrowers see on their home equity loans.

- Changes in the federal funds rate can lead to changes in the prime rate, which is often used as a benchmark for home equity loan rates.

- Government housing policies, such as programs aimed at promoting homeownership or stabilizing the housing market, can also impact the availability and pricing of home equity loans.

- Regulatory changes in response to economic conditions or financial crises can have a ripple effect on the lending environment, affecting interest rates and loan terms.

Evaluating the impact of credit history on 5-year home equity loan rates

When it comes to 5-year home equity loan rates, credit history plays a significant role in determining the interest rates offered by lenders. Borrowers with a strong credit history are likely to secure lower interest rates, while those with poor credit may face higher rates or even difficulty in obtaining a loan.

How Credit History Affects Loan Rates

Credit history is a reflection of a borrower’s financial responsibility and risk level. Lenders use credit scores to assess the likelihood of timely repayment. A higher credit score indicates lower risk, leading to lower interest rates. On the other hand, a lower credit score suggests higher risk, resulting in higher interest rates or loan denial.

Tips for Improving Credit Scores

– Pay bills on time to build a positive payment history.

– Keep credit card balances low and avoid maxing out credit limits.

– Regularly check credit reports for errors and dispute inaccuracies.

– Limit new credit applications to prevent multiple inquiries that can lower scores.

Strategies for Borrowers with Less-Than-Perfect Credit

Borrowers with less-than-perfect credit can still secure favorable rates by:

– Providing a larger down payment to reduce the loan amount.

– Seeking a co-signer with a strong credit history.

– Exploring loan options from credit unions or local banks that may consider alternative factors beyond credit scores.

| Credit Score Range | Interest Rate (%) |

|---|---|

| Excellent (750+) | 3.25% |

| Good (700-749) | 3.75% |

| Fair (650-699) | 4.50% |

| Poor (600-649) | 5.25% |

| Very Poor (Below 600) | 6.00% |

An example of how a specific credit score can translate to a higher or lower interest rate: A borrower with a credit score of 780 may qualify for a 3.00% interest rate, while a borrower with a credit score of 620 could face a 5.50% interest rate.

Forecasting future trends in 5-year home equity loan rates

In the ever-changing landscape of home equity loan rates, predicting future trends is crucial for borrowers to make informed decisions. By analyzing economic factors and historical data, we can gain insights into what the future may hold for 5-year home equity loan rates.

Impact of Economic Factors on 5-year Home Equity Loan Rates

- Economic factors such as inflation and interest rates play a significant role in determining home equity loan rates. As inflation rises, lenders may adjust rates to maintain profitability.

- Housing market conditions also influence loan rates, with a booming market potentially leading to higher rates due to increased demand.

Analyzing Historical Data for Future Rate Predictions

- Studying historical data on loan rates can reveal cyclical patterns or trends that may help forecast future rates. By identifying past fluctuations, we can anticipate potential shifts in the market.

- Utilizing machine learning models or statistical analysis can provide more accurate predictions of future 5-year home equity loan rates based on various scenarios and market conditions.

Comparative Analysis of Fixed vs. Variable Rates

- Comparing fixed-rate and variable-rate home equity loans can help borrowers determine which option may be more suitable in the future. Fixed rates offer stability, while variable rates may fluctuate with market conditions.

Key Factors Influencing Future 5-year Home Equity Loan Rates

- Creating a detailed report outlining the key factors influencing 5-year home equity loan rates is essential for individuals considering such loans in the upcoming years. Factors like economic indicators, market trends, and regulatory changes all play a role in rate determination.

Closure

From understanding APR to evaluating market trends and refinancing options, this guide has covered a wide array of topics related to 5-year home equity loan rates. Whether you’re a first-time borrower or looking to refinance, the information presented here aims to empower you to make informed decisions and secure the most favorable terms for your financial future.