Delving into lowest home equity loan rates, this introduction immerses readers in a unique and compelling narrative. Exploring the factors affecting rates, types of loans available, and strategies to secure the best rates, this guide offers valuable insights for homeowners seeking affordable financing options.

Factors affecting home equity loan rates

When considering a home equity loan, it’s essential to understand the various factors that can influence the interest rates offered by lenders. These factors play a crucial role in determining the overall cost of borrowing and can significantly impact your financial decisions.

Credit Score

Your credit score is one of the most significant factors that lenders consider when determining the interest rate for a home equity loan. A higher credit score typically results in lower interest rates, as it indicates to lenders that you are a lower credit risk. Conversely, a lower credit score may lead to higher interest rates or difficulty in securing a loan.

Loan Amount and Term

The loan amount and term also play a role in determining home equity loan rates. Generally, larger loan amounts or longer loan terms may result in higher interest rates, as they pose a greater risk to lenders. On the other hand, smaller loan amounts and shorter terms may lead to lower interest rates.

Economic Conditions and Market Trends

Economic conditions and market trends can impact the fluctuation of home equity loan rates. For example, during periods of economic uncertainty or rising interest rates, lenders may increase their rates to mitigate risks. Conversely, in a stable economy with low-interest rates, borrowers may benefit from lower rates.

Lender’s Policies and Borrower’s Financial History

The lender’s policies and the borrower’s financial history also play a crucial role in determining the lowest home equity loan rates. Lenders may offer preferential rates to borrowers with a strong financial history and stable income. Additionally, the lender’s policies, such as fees and requirements, can influence the overall cost of borrowing.

| Credit Score | Interest Rate Range |

|---|---|

| Excellent | 3.25% – 4.5% |

| Good | 4.5% – 6% |

| Fair | 6% – 8% |

| Poor | 8% – 10% |

A scenario where a change in the loan amount resulted in a significant shift in the offered interest rate for a home equity loan: Increasing the loan amount from $50,000 to $100,000 led to a rise in the interest rate from 4.5% to 5.75%.

Short-term vs. Long-term Loan Impact

When comparing the impact of a short-term versus a long-term loan on the total cost of borrowing for a home equity loan, it’s essential to consider the interest rates and repayment periods. For example, a $50,000 loan with a 5% interest rate over 5 years would have a total cost of borrowing of $11,289, while the same loan over 10 years would result in a total cost of $21,416, showcasing the higher cost of a long-term loan.

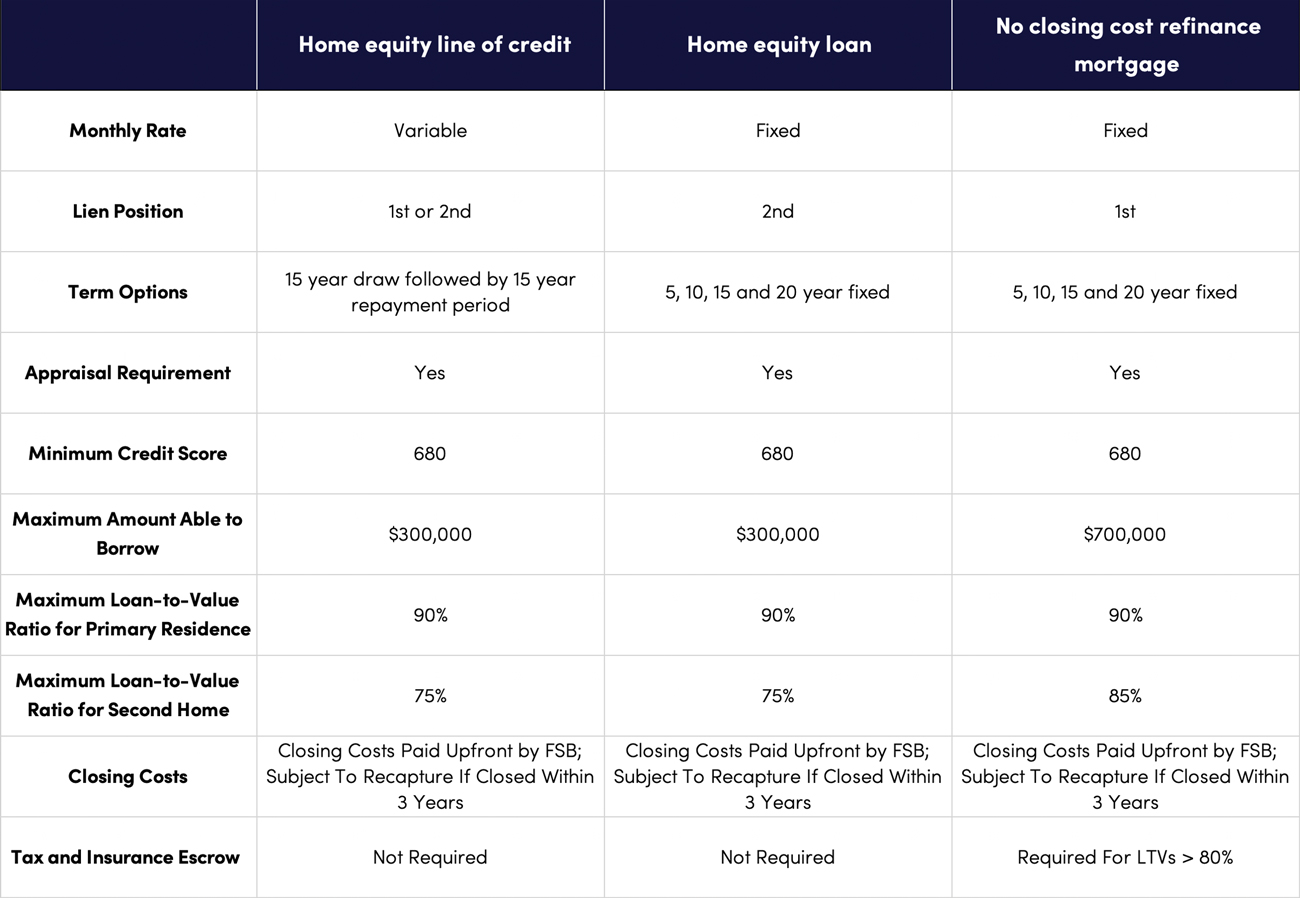

Types of home equity loans available

When considering a home equity loan, it’s important to understand the different types available to determine which option best suits your financial needs and goals. Two common types of home equity loans are fixed-rate and variable-rate loans.

Differences between fixed-rate and variable-rate home equity loans

- A fixed-rate home equity loan offers a consistent interest rate throughout the life of the loan, providing predictability in monthly payments.

- On the other hand, a variable-rate home equity loan has an interest rate that can fluctuate based on market conditions, potentially leading to lower initial rates but higher risk of payment increases in the future.

Advantages and disadvantages of a home equity loan versus a home equity line of credit (HELOC)

- A home equity loan provides a lump sum upfront with a fixed interest rate and predictable monthly payments, making it ideal for one-time expenses like home renovations.

- In contrast, a HELOC operates more like a credit card with a revolving line of credit, allowing you to borrow as needed up to a certain limit while only paying interest on the amount borrowed.

- While a home equity loan may offer lower interest rates, a HELOC provides flexibility and the ability to access funds over time.

Cash-out refinance vs. traditional home equity loan

- A cash-out refinance replaces your existing mortgage with a new one for a larger amount, allowing you to access the equity in your home while potentially securing a lower interest rate.

- On the other hand, a traditional home equity loan allows you to borrow against the equity in your home without refinancing your entire mortgage.

- Depending on current market rates and your financial goals, a cash-out refinance may offer better terms and rates compared to a traditional home equity loan.

Strategies to secure the lowest home equity loan rates

Securing the lowest home equity loan rates involves a combination of factors that borrowers can leverage to their advantage. By focusing on improving credit scores, negotiating with lenders, and timing their application correctly, borrowers can increase their chances of securing the best rates available in the market.

Improving Credit Score

One of the most effective ways to secure lower home equity loan rates is by improving your credit score. Lenders use credit scores to assess the risk of lending to a borrower, with higher scores typically leading to better rates. To boost your credit score, make sure to pay bills on time, keep credit card balances low, and avoid opening new lines of credit unnecessarily.

Negotiation Strategies

When applying for a home equity loan, don’t be afraid to negotiate with lenders to secure better rates. Research current market rates and use this information to leverage a better deal. Highlight your strong credit score, financial stability, and loyalty to the lender to negotiate for reduced rates or additional benefits.

Timing Strategies

Timing can also play a crucial role in securing the lowest home equity loan rates. Keep an eye on market trends and interest rate movements to apply for a loan when rates are at their lowest. Additionally, consider consolidating debt or improving your financial profile before applying to increase your chances of qualifying for the best rates available.

Comparison of different lenders offering low home equity loan rates

When looking for a home equity loan, it’s crucial to compare different lenders to ensure you’re getting the best deal possible. Below is a detailed comparison of the top 5 lenders known for offering competitive low home equity loan rates.

Lender Comparison Table

| Lender | Interest Rate | Loan Terms | Eligibility Requirements | Special Features/Benefits |

|---|---|---|---|---|

| Lender A | 3.25% | Up to $200,000, 15-year term | Credit score 680+, DTI ratio <45% | No closing costs |

| Lender B | 3.50% | Up to $150,000, 20-year term | Credit score 700+, DTI ratio <50% | Flexible payment options |

| Lender C | 3.75% | Up to $250,000, 10-year term | Credit score 720+, DTI ratio <40% | Low origination fees |

| Lender D | 3.45% | Up to $180,000, 15-year term | Credit score 690+, DTI ratio <48% | Fast approval process |

| Lender E | 3.60% | Up to $220,000, 12-year term | Credit score 700+, DTI ratio <45% | Rate discounts for existing customers |

Online Lenders vs. Traditional Banks and Credit Unions

Online lenders often offer lower interest rates and quicker approval processes compared to traditional banks and credit unions. However, traditional institutions may provide better customer service and more personalized guidance throughout the loan process.

Key Factors to Consider When Selecting a Lender

- Compare interest rates, fees, and repayment terms to find the most cost-effective option.

- Consider the lender’s eligibility requirements and ensure you meet the necessary criteria.

- Look for special features like no closing costs or flexible payment options that align with your financial goals.

- Evaluate customer service reviews and the overall experience of working with each lender.

- Choose a lender that offers a combination of low rates, favorable terms, and excellent customer support to meet your needs.

Understanding the APR and interest rates for home equity loans

When considering a home equity loan, it’s crucial to understand the difference between APR and interest rates, as they directly impact the overall cost of the loan.

Difference Between APR and Interest Rates

Interest rate refers to the percentage of the loan amount charged by the lender for borrowing the money. On the other hand, APR (Annual Percentage Rate) includes not only the interest rate but also any additional fees or costs associated with the loan, giving a more comprehensive view of the total cost.

Impact of Lower Interest Rate on Overall Cost

While a lower interest rate may initially seem beneficial, it’s essential to consider associated fees and closing costs. In some cases, a loan with a lower interest rate may have higher fees, resulting in a higher overall cost compared to a loan with a slightly higher interest rate and lower fees.

Effect of Introductory Rates and Promotional Offers

Introductory rates and promotional offers can entice borrowers with lower initial rates. However, it’s important to evaluate how these rates will adjust over time and consider the long-term affordability of the loan beyond the introductory period.

Comparison of Home Equity Loan Offers

| Lender | APR | Interest Rate | Fees | Closing Costs |

|---|---|---|---|---|

| Lender A | 4.5% | 4.0% | $500 | $2,000 |

| Lender B | 4.2% | 4.2% | $700 | $1,800 |

| Lender C | 4.8% | 4.5% | $600 | $2,200 |

Compound Interest and Total Amount Repaid

Compound interest refers to the interest calculated on the initial principal and also on the accumulated interest from previous periods. This can significantly impact the total amount repaid over the loan term, especially for longer loan durations.

Calculation of Monthly Payments

Monthly payments for a home equity loan are typically calculated based on the principal amount borrowed, the interest rate, and any additional fees. The monthly payment consists of a portion of the principal amount, interest, and fees, with the proportion of each varying over the loan term.

Risks associated with low home equity loan rates

When considering low home equity loan rates, it is important to be aware of the potential risks that may come with them. While these rates can be attractive, they may not always be the best option for every borrower. Here are some key risks to keep in mind:

Variable rates

- Low home equity loan rates may be variable, meaning they can fluctuate based on market conditions. This can lead to unpredictable monthly payments and potential financial strain if rates increase significantly.

- It is essential to understand the terms of the loan and how often the rate can adjust to ensure you can afford potential payment increases in the future.

Balloon payments

- Some low home equity loans may have balloon payments, requiring borrowers to pay off the remaining balance in a lump sum at the end of the loan term.

- If you are not prepared for this large payment, it can lead to financial difficulties or the risk of losing your home.

Prepayment penalties

- Opting for a low home equity loan rate with prepayment penalties can restrict your ability to pay off the loan early or refinance without incurring additional fees.

- These penalties can negate any potential savings from a low rate, so it’s important to consider the long-term implications before committing to a loan with such terms.

Economic changes and housing market fluctuations

- Changes in the economy and fluctuations in the housing market can impact borrowers with low home equity loan rates.

- If property values decline or economic conditions worsen, borrowers may find themselves owing more on their loan than their home is worth, creating challenges in selling or refinancing.

Financial prudence in decision-making

- While low home equity loan rates can be enticing, there are scenarios where opting for the lowest rate may not be the most financially prudent decision.

- For example, if you plan to move or sell your home in the near future, the costs associated with refinancing or selling with a low rate may outweigh the benefits.

Qualifications required to access the lowest home equity loan rates

To access the lowest home equity loan rates, borrowers need to meet specific qualifications set by lenders. These qualifications typically include factors such as credit score, debt-to-income ratio, and loan-to-value ratio, among others.

Minimum Credit Score and Financial Stability

- A minimum credit score is often required to qualify for the lowest home equity loan rates. Lenders typically look for a credit score of 700 or higher.

- Income stability and employment history play a crucial role in demonstrating financial stability and improving eligibility for low rates.

- Borrowers with a lower debt-to-income ratio are more likely to qualify for the lowest rates as it shows their ability to manage debt responsibly.

Property Value and Home Equity Amount

- The value of the property and the amount of equity the borrower has in the home are significant factors in determining eligibility for low rates.

- Lenders may require a specific loan-to-value ratio to qualify for the lowest rates, with lower ratios indicating less risk for the lender.

- Having a substantial amount of home equity in relation to the loan amount sought can increase the chances of accessing the lowest rates.

Self-Employed Individuals and Non-Traditional Income Sources

- Self-employed individuals or those with non-traditional income sources can qualify for low home equity loan rates by providing documentation such as tax returns, profit and loss statements, and bank statements to verify income stability.

- Showing a consistent income stream and financial responsibility can help self-employed borrowers secure the lowest rates.

Co-Signer and Additional Collateral

- Having a co-signer with a strong credit history or providing additional collateral can improve eligibility for the lowest home equity loan rates.

- A co-signer takes on the responsibility of the loan if the borrower defaults, reducing the risk for the lender and potentially leading to lower rates for the borrower.

Benefits of securing the lowest home equity loan rates

Securing the lowest home equity loan rates can greatly benefit borrowers in various ways. By obtaining a loan with the lowest rates, homeowners can enjoy lower monthly payments and save a significant amount on overall interest costs throughout the life of the loan.

Lower Monthly Payments and Interest Savings

- Lower interest rates translate to reduced monthly payments, making it easier for borrowers to manage their finances.

- By securing the lowest rates, homeowners can save thousands of dollars in interest over the term of the loan compared to higher rate options.

- Reduced interest payments mean more money in the borrower’s pocket to allocate towards other financial goals or expenses.

Affordable Financing Options for Large Expenses

- Accessing low home equity loan rates provides homeowners with a cost-effective way to finance major expenses such as home renovations, education costs, or medical bills.

- Lower rates mean lower borrowing costs, allowing borrowers to tackle big projects without breaking the bank.

- Securing the lowest rates can make it easier for homeowners to access the funds they need for significant investments or purchases.

Debt Consolidation and Financial Improvement

- Refinancing with lower rates can help borrowers consolidate high-interest debt into a single, more manageable monthly payment.

- By using a home equity loan to pay off credit cards or other debts, borrowers can streamline their finances and potentially improve their credit score.

- Consolidating debt with a low-rate home equity loan can lead to long-term financial stability and savings on interest costs.

Impact of home equity loan rates on financial planning

When it comes to financial planning, home equity loan rates play a crucial role in shaping the overall strategy of homeowners. Fluctuations in these rates can significantly impact long-term financial goals and objectives. Homeowners need to carefully consider the impact of these rates on their financial planning to make informed decisions.

Incorporating home equity loans with low rates into financial plans

Utilizing home equity loans with low rates can be a strategic move in achieving financial stability and growth. By incorporating these loans into a comprehensive financial plan, homeowners can leverage their home equity to fund various endeavors such as home improvements, debt consolidation, or investments. This can help optimize their financial resources and achieve their long-term goals more efficiently.

- Low home equity loan rates can provide homeowners with access to additional funds at a lower cost, allowing them to pursue investments with higher returns.

- By using home equity loans with low rates for debt consolidation, homeowners can streamline their finances and potentially save on interest payments, contributing to long-term financial health.

- Homeowners can strategically allocate funds from home equity loans with low rates towards retirement savings or education funding, ensuring a more secure financial future.

Leveraging home equity for financial goals

When homeowners leverage their home equity with the lowest rates available, they can accelerate the achievement of their financial goals. Whether it’s saving for retirement, funding education, or investing in property, home equity loans with low rates can provide the necessary financial resources to make these aspirations a reality.

- Opting for home equity loans with low rates can help homeowners maximize their borrowing capacity while minimizing interest expenses, creating a more cost-effective financial strategy.

- By strategically utilizing low-rate home equity loans, homeowners can diversify their investment portfolio, increase their net worth, and build a more robust financial foundation for the future.

- Home equity loans with low rates can serve as a valuable tool for homeowners to optimize their financial planning, enabling them to achieve their long-term objectives with greater ease and efficiency.

Regulatory considerations and consumer protection for low home equity loan rates

When it comes to low home equity loan rates, regulatory considerations and consumer protection play a vital role in ensuring that borrowers are treated fairly and transparently in the lending process.

Role of Government Agencies

Government agencies such as the Consumer Financial Protection Bureau (CFPB) are responsible for monitoring and enforcing fair lending practices in the home equity loan market. They oversee that lenders adhere to regulations designed to protect consumers from predatory practices.

Consumer Rights and Disclosures

- Borrowers have the right to receive clear and accurate information about the terms and conditions of their home equity loan, including interest rates, fees, and repayment terms.

- Lenders must provide borrowers with a Loan Estimate and Closing Disclosure outlining all costs associated with the loan.

Comparison between Fixed-rate and Variable-rate Loans

| Aspect | Fixed-rate Loan | Variable-rate Loan |

|---|---|---|

| Interest Rate Fluctuations | Stable interest rate throughout the loan term | Interest rate can change periodically |

| Repayment Terms | Predictable monthly payments | Payments may vary based on interest rate changes |

| Overall Cost | Higher initial rate but offers consistency | Potentially lower initial rate but subject to increases |

A real-life scenario where a borrower faced hidden fees in a home equity loan agreement: “Despite being promised a low interest rate, the borrower discovered additional fees buried in the fine print, significantly increasing the total cost of the loan.”

Calculating Total Cost of a Home Equity Loan

To calculate the total cost of a home equity loan, borrowers should consider factors such as interest rates, closing costs, and potential prepayment penalties. Use the following formula: Total Cost = Loan Amount + Interest + Fees.

Red Flags for Borrowers

- Offers with unusually low introductory rates that skyrocket after a short period.

- Complex adjustable rate structures that make it challenging to predict future payments.

Trends in the home equity loan market affecting rates

The home equity loan market is subject to various trends that can impact the interest rates offered to borrowers. Understanding these trends is crucial for individuals seeking to secure the best possible rates for their home equity loans.

Rising Interest Rates and Home Price Appreciation

In a climate of rising interest rates, borrowers may find that home equity loan rates also increase. This is often influenced by the Federal Reserve’s monetary policy and overall economic conditions. Additionally, as home prices appreciate, borrowers may have access to more equity in their homes, potentially affecting the rates offered by lenders.

Technological Advancements and Digital Platforms

Advancements in technology have streamlined the home equity loan process, making it easier for borrowers to compare rates and secure loans online. Digital platforms have enabled borrowers to access a wider range of lenders and offers, increasing competition and potentially leading to better rates.

Changing Demographics and Generational Preferences

Demographic shifts and generational preferences can also impact the home equity loan market. For example, younger generations may have different attitudes towards borrowing and homeownership, influencing the types of loan products and rates available in the market.

Government Policies and Regulations

Government policies and regulations play a significant role in shaping home equity loan rates. Changes in legislation, such as tax laws or consumer protection measures, can impact interest rates and borrowing conditions. It is essential for borrowers to stay informed about these developments.

Fixed-Rate vs. Variable-Rate Home Equity Loans

When considering home equity loans, borrowers must weigh the pros and cons of fixed-rate and variable-rate options. Fixed-rate loans offer stability in interest rates, while variable-rate loans may fluctuate with market conditions. Understanding these differences is crucial in determining the most suitable loan for individual needs.

Credit Scores and Financial History

Credit scores and financial history play a significant role in determining the interest rates offered for home equity loans. Borrowers with higher credit scores and a strong financial track record are more likely to secure lower rates. Improving creditworthiness through responsible financial management can help borrowers access better loan terms.

How to calculate the total cost of a home equity loan with low rates

When considering a home equity loan with low rates, it is crucial to calculate the total cost involved. This includes factoring in interest rates, fees, and repayment terms to determine the most cost-effective option.

Factors to Consider for Total Cost Calculation

- Start by gathering loan offers from different lenders, noting the interest rates, annual fees, closing costs, and any other charges associated with the loan.

- Consider the repayment terms, including the loan duration and whether it is a fixed-rate or adjustable-rate loan, as this can impact the total cost over time.

- Review the amortization schedule provided by the lender to understand how much of each payment goes towards interest versus the principal balance.

- Be aware of any potential hidden costs, such as prepayment penalties or balloon payments, which can significantly impact the total cost of the loan.

Using a Loan Repayment Calculator

- Utilize a loan repayment calculator to estimate your monthly payments based on the loan amount, interest rate, and repayment term.

- Calculate the total interest paid over the life of the loan by multiplying the monthly payment by the total number of payments and subtracting the loan amount.

- Adjust the loan parameters in the calculator to compare different loan offers and determine which one offers the lowest total cost.

Negotiating for Better Terms

- Don’t hesitate to negotiate with lenders to secure lower interest rates or reduced fees, especially if you have a strong credit history or valuable assets to offer as collateral.

- Compare offers from multiple lenders and use the information gathered to leverage better terms during the negotiation process.

- Be prepared to ask questions and seek clarification on any terms or conditions that may affect the total cost of the loan.

Case studies or success stories of individuals benefiting from low home equity loan rates

In the following sections, we will explore real-life examples of how homeowners have utilized low home equity loan rates to achieve their financial objectives and enhance their overall financial well-being.

Case Study 1: The Smith Family

The Smith family, consisting of John and Sarah Smith, were looking to renovate their outdated kitchen but were concerned about the high costs involved. By leveraging a low home equity loan rate offered by their trusted lender, they were able to access the funds needed at a favorable interest rate. This allowed them to complete the renovation project within their budget and increase the value of their home significantly.

Case Study 2: Mary Johnson

Mary Johnson, a single mother of two, was facing unexpected medical expenses and needed financial support. She decided to explore the option of a home equity loan with low rates to cover the medical bills without compromising her long-term financial stability. With careful planning and the guidance of a financial advisor, Mary secured a low-rate home equity loan that provided the necessary funds while keeping her monthly payments manageable.

Case Study 3: The Patel Family

The Patel family had been dreaming of sending their children to college but were concerned about the high tuition costs. By taking advantage of a low home equity loan rate, they were able to access the funds needed to cover the education expenses without dipping into their savings or retirement accounts. This strategic decision not only helped their children pursue higher education but also ensured the family’s financial future remained secure.

Future outlook for home equity loan rates and predictions

The future outlook for home equity loan rates is subject to various factors that can influence the direction in which rates may go. Economic forecasts, regulatory changes, and market indicators all play a role in determining the trajectory of home equity loan rates in the coming years.

Factors influencing future home equity loan rates

- Economic conditions: The overall health of the economy, including inflation rates, employment levels, and GDP growth, can impact home equity loan rates. A strong economy may lead to higher rates, while a weaker economy could result in lower rates.

- Regulatory changes: Any new regulations or policies implemented by governing bodies can affect lending practices and interest rates. Changes in the regulatory environment could lead to fluctuations in home equity loan rates.

- Market trends: Supply and demand dynamics in the housing market, as well as investor sentiment, can influence the direction of home equity loan rates. Changes in market conditions can impact the cost of borrowing for homeowners.

Ending Remarks

In conclusion, understanding the nuances of home equity loan rates is crucial for making informed financial decisions. By comparing lenders, exploring different loan options, and leveraging the benefits of low rates, homeowners can secure the best financing for their needs.